Interest-Free Days Credit Cards

A few years ago when I wrote this guide, the average interest rate was 14.49% p.a. Now, it’s 20.99% and climbing. Some interest rates today are hitting nearly 30% p.a..

These kinds of numbers show us that avoiding interest is critical if you want to use your credit safely and avoid money traps. Luckily - and somewhat strangely - credit cards come with a built-in safety mechanism to help you avoid interest altogether.

They’re called interest free days. There are two types of interest free days, and we’ll distinguish both and show you how to utilise them best. Our goal is to help you find a credit card that not only gives you the most helpful, money-saving features, but also keeps you clear of the interest snowball.

You’ll need to know:

- The types of interest free days

- How to use them strategically

- How “up to” works on the statement calendar

- How to compare cards to find a good one for you

Best interest free credit cards

First, we’re going to make it easy to see how interest free cards work for different lifestyles and the cost-benefit trade-off. That way, you can easily pinpoint the type of card you need.

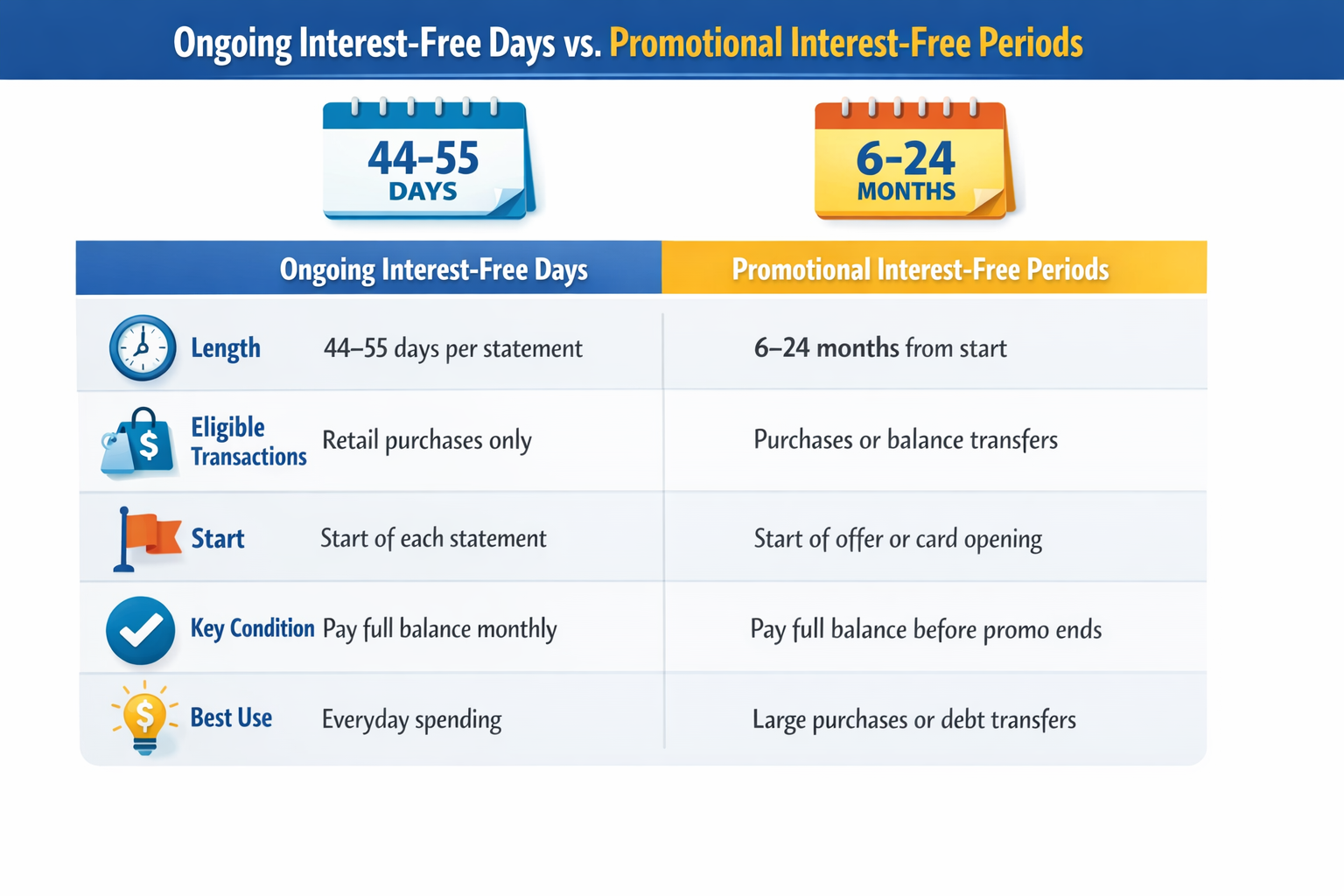

First, we need to explain ongoing interest free days versus promotional periods.

There are two main types of interest free periods on credit cards: ongoing interest free days, and promotional interest free periods.

We’ll break down each one so you can see how they differ.

Promotional interest-free periods

These promotions temporarily suspend interest charges for a period of time as a new customer promotion, usually 6, 12 or even 24 months. During that time, you won’t be charged interest on purchases, even if you don’t pay the balance off in the statement period.

So, for example:

You get a card with 0% p.a. on purchases for 12 months and spend $3000. As long as the interest-free offer is active, no interest is charged. After the 12 month promotion ends, any remaining debt is charged interest at the card’s

normal rate (so you should pay it off before then).

Ongoing interest free days

Standard interest free days are an ongoing feature of the card. Most cards include up to 44 or 55 interest-free days, but only if you pay your closing balance in full by the due date. Some cards will void any interest-free days when you have a balance transfer, which means you’ll pay interest on purchases immediately.

For example:

You spend $1500 on your card in your statement period. If you pay the full amount off by the due date, you won’t pay any interest at all.

⚠️ This is important!

The 44 or 55 interest-free days don’t start from the day you make a purchase. They start from the beginning of your statement period.

For example:

If your statement period is 30 days and your card offers 55 interest-free days:

A purchase made on day 1 will get close to the full 55 days interest-free.

A purchase made on day 30 only has around 25 days interest-free until the payment due date.

The bottom line is that as long as you pay the full statement balance by the due date, all purchases in that period remain interest-free, even though each purchase technically gets a different number of days.

Strategically using 44 or 55 days interest free

You can time purchases to make the most of the standard interest-free period on your card (typically 44 or 55 days), because items purchased earlier in the statement period will give you more time to save up the funds to pay the statement in full when it’s due.

For instance, if you bought a $300 chair on day 1 of your 30-day statement period and the card includes 55 days interest free, you’ll have close to 55 days to save the cash to pay it off in full.

By comparison, if you bought the chair on day 30, you would only have 15 days to save before being charged interest.

When you use interest-free days strategically like this, you can avoid being one of the 49.8% of Aussies (that’s almost half) whose credit cards are accruing interest right now.

The bottom line: larger purchases or expenses can possibly be timed closer to the beginning of a new statement period to allow more time to pay it off.

If you don’t pay off the card in full (i.e., you carry a balance over to the next statement period), or you miss a payment, you’ll be charged interest immediately on new purchases.

Paying your card off completely each statement period = no interest charges.

Strategically using promotional interest free periods

Promotional interest free periods (such as 0% on purchases for 6, 12 or 24 months) start from when the card is opened, not each statement period like ongoing interest-free days. So, purchases made during the 0% offer all have the same end-date.

Strategically, you can use this kind of offer to make a big purchase and pay it off over time. If it’s paid offIf it’s not paid off, you’ll be charged the card’s standard rate on whatever balance remains (which is what the banks are hoping for).

That means promotional interest-free periods are often great for:

- Large expenses such as new furniture, holidays and big bills you need time to pay off

- Spreading the repayments out without paying interest

- Controlling cashflow for a short period

The bottom line: 0% interest offers help you manage big costs without paying extra in interest. They are not a ticket to free money.

Since you’re charged interest on any remaining balance after the 0% promotion finishes, it’s very important to:

- Know the exact end date of the offer

- Set a repayment plan to clear the balance in time

- Avoid adding new purchases close to the end of the promotional period

Being strategic about when you make big purchases is even more important during peak purchasing seasons like Christmas. In December 2025, Aussies had racked up a record $28 billion in personal credit card debt, accruing interest up to $17.8 billion. That’s scary enough to make boring old interest worth understanding.

What isn’t covered under interest-free periods?

Both kinds of interest-free periods (ongoing and promotional) are designed for everyday purchases, not cash advances.

Cash advances are generally a poor idea because they’re treated very differently by lenders than a regular purchase. Cash advances include ATM withdrawals from your credit card, gambling transactions and transfers from your card to a bank account.

Cash advances:

- Don’t receive any interest-free period

- Start accruing interest from the day the transaction is made

- Often attract a higher interest rate than purchases, called the cash advance rate

- May also slap you with a cash advance fee

Comparing interest-free credit cards against other features

The interest-free period is only one factor on a credit card. To find the best one for you, you’ll need to compare other features like annual fees, rewards points and additional benefits. These can significantly affect the value of your credit card and how you use.

To make this simpler, we’ve outlined below the kinds of goals you might have for your credit card, and what to think about when comparing.

| If you’re after… | Then consider… |

|---|---|

| A long interest-free period to pay off a large purchase | A higher annual fee might reduce your savings. Rewards points are less important if you’re not using the card for ongoing purchases. |

| Everyday spending with ongoing interest-free days | Look for a card with no or low annual fees, a strong rewards program, and ongoing perks like purchase protection or travel insurance. |

| Maximising rewards points | Choose a card with a good points program or cashback, even if the interest-free period is shorter, and pay balances in full each month to avoid interest. |

| Access to extra benefits (insurance, concierge, travel perks) | Make sure the card offers the benefits you actually use — some promo-focused cards limit these during the interest-free period. |

| Flexible budgeting and short-term cash flow | A card with ongoing interest-free days or shorter promotional periods can help you manage month-to-month spending without paying interest. |

Popular credit cards with 44, 45 and 55 days interest free

Qantas American Express Ultimate credit card

The Qantas American Express Ultimate Credit Card offers up to 44 interest‑free days on purchases if you pay your statement in full each month, which helps avoid interest while you rack up points. It earns Qantas Points which is ideal if rewards and travel perks are a priority.

Suited for: people who spend enough to justify the fee rather than those solely chasing the interest‑free feature, since it has a high annual fee and premium benefits.

NAB Low Rate credit card – Cashback Offer

The NAB Low Rate credit card with a cashback offer typically includes up to 55 interest‑free days on purchases, plus a cashback bonus if you meet the spend criteria in the intro period. Its relatively low ongoing purchase rate and nifty cashback offer make it practical for everyday spending while still getting a good amount of interest‑free time.

Suited for: people who want low borrowing costs and a small upfront cash benefit without focusing on rewards points.

American Express Explorer credit card

The American Express Explorer Credit Card comes with up to 55 interest‑free days on purchases, which is helpful if you pay off each month and want to manage cash flow effectively. It also earns Membership Rewards points and includes travel credits and insurance, adding value if you use the card for travel or planned spending.

Suited for: people who will spend enough to benefit from both the rewards and interest‑free features, since it has a higher annual fee.

The Westpac Lite Mastercard provides up to 45 interest‑free days on purchases while charging a low monthly fee and 0% foreign transaction fees, which can be especially helpful for international spending. Its lower interest rate and simple structure make it a solid choice for everyday use and travellers who want to avoid foreign transaction costs while still enjoying interest‑free days.

Suited for: people who want an affordable, straightforward card with cost‑saving features rather than big rewards.

American Express Velocity Escape Plus card

The American Express Velocity Escape Plus Card offers up to 55 interest‑free days on purchases, which is useful for everyday spend if you’re disciplined about paying in full each month. It also earns Velocity Points and includes travel insurance, making it attractive for Virgin Australia flyers or frequent travellers who want points alongside the interest‑free feature.

Suited for: people who want both points and interest‑free flexibility, since it offers decent travel benefits for a modest annual fee.

Other credit cards to consider

There are other options that can help you save on your credit card if interest-free days aren’t a priority, or if you have a large sum to pay down. You could consider:

These allow you to move existing credit card debt from one card to another and often come with a promotional 0% interest‑free period on the transferred balance. This can save you interest while you pay down what you owe, but there may be a balance transfer fee. You might also pay for interest immediately on new purchases. These cards are a good choice if you carry debt now and want to reduce interest costs, but you’ll need a plan to clear the balance before the promo ends to avoid high interest afterward.

While they may not have long promotional offers, low interest rate cards offer a consistently lower ongoing purchase rate than most standard cards. That means if you occasionally carry a balance from month to month, you’ll pay less interest on that carried balance compared with a typical card. These cards are best for people who know they won’t always pay in full and want to minimise interest charges over time rather than chase interest‑free days.

Low annual fee cards keep the ongoing cost of holding the card down, but it’s likely you’ll get fewer rewards in return. Many of these cards still include standard interest‑free days on purchases if you pay the statement in full, but they won’t usually have large sign‑on bonuses or premium benefits. These cards are ideal if your priority is keeping fees low while still getting the core benefits of a credit card, especially if you pay off your balance regularly and don’t need high‑end perks.

The easy guide to how credit card interest works

If you’re reading the word “interest” over and over and you’re not sure how it works, we’ll explain it here.

When you use your credit card, you are essentially borrowing money from your card provider to cover the purchase you are making. Interest is the cost your card provider charges for providing this service.

How credit card interest is calculated can vary according to the card provider, but for the most part, interest is calculated from the day each transaction is made, up until the day it is repaid in full (unless an interest-free period comes into play).

At the end of the statement period, interest is calculated by averaging the amount borrowed each day, and then multiplying that amount by the rate set out in your card’s terms. Interest charges are calculated separately for purchases, cash advances, and balance transfers.

Breaking it down, your card provider will:

- Average the balance over the statement period,

- Multiply the average balance by the applicable daily interest rate (which is the annual rate divided by 365),

- Then multiply the above amount by the number of days in the statement period.

The step-by-step process to choosing a card with interest-free days

Finding a credit card and applying is a simple process, although it may take some time to compare cards to find the right one. After that, you need to follow the formula to stay interest-free. Here’s what that process looks like:

Step 1. Choose the right card. First and foremost, compare the options to choose the right card. Take into account what you need from a card, then find the card that suits your needs and your budget. Look at how many interest-free days your card offers. While some options offer no interest-free days, most range between 44 and 55 days.

Step 2. Read the small print. While it’s always important to read the small print before you apply, it’s a good idea to check over the important bits again before you start using the card. This includes finding out exactly how your card deals with interest-free days. Check when your statement period starts and ends, and how long you have before your payment is due.

Step 3. Plan your purchases. If you know you need to make a larger purchase, it can be a good idea to do it at the start of your statement period, as that will give you longer before your payment is due. You can always track your purchases using your card’s app so that you know where you stand and how much you owe.

Step 4. Always pay off your balance. If you want to take advantage of your card’s interest-free days, the most important thing to remember is to pay your closing balance by the due date each month. If you are unable to do that once in a while, at least make your minimum repayment.

When you’re able, clear your balance to get back on track with your interest-free days. You don’t need to wait until your next statement due date to do this, you can do it at any time. The sooner you do pay off your balance, the sooner that balance stops accruing interest, which should save you money in the long run.

FAQs

Q. Why do cards say 'up to' 55 days interest-free?

A. The term 'up to' is used because the actual number of interest-free days depends on when you make a purchase during your statement. If you make a purchase on day 1 of your statement period, you’ll have 55 days interest free, but a purchase on day 20 will only have 25 days interest free.

Q. Do cash advances have interest-free days?

A. No, interest-free days don’t apply to cash advances and interest is typically charged from the date of the withdrawal or transaction.

Q. Does a balance transfer affect my interest-free period for new purchases?

A. Yes, having an outstanding balance transfer can often void the interest-free period on new purchases unless your bank offers a specific 'Interest-Free Days Payment' option. Many Aussie lenders require you to pay the entire closing balance including the transferred amount to maintain the interest-free window on your daily spending.

Q. Are BPAY payments eligible for interest-free days?

A. Yes, most BPAY payments are treated as standard purchases and qualify for the interest-free period. However, payments to certain billers such as financial institutions or for 'cash-like' transactions may be treated as cash advances which incur interest and fees immediately.

Q. Can I get interest-free days on ATO tax payments?

A. Yes, payments made to the Australian Taxation Office (ATO) using a credit card generally qualify for interest-free days because they are processed as purchase transactions. Just note that the ATO applies its own credit card surcharge and many banks exclude these payments from earning reward points.

Q. How do I regain interest-free days after failing to pay the full balance?

A. You can regain your interest-free days by paying the full closing balance shown on your statement by the due date in a subsequent billing cycle. Once you have cleared the outstanding debt in full, new purchases in the following statement period will typically benefit from the interest-free grace period again.

Q. What happens to my interest-free period if I only make the minimum repayment?

A. You will lose your interest-free days for the current statement and usually for the subsequent statement cycle as well. Interest will be charged on your outstanding balance and any new purchases from the day they are made until the entire closing balance is paid in full.

Q. Do interest-free days apply to international transaction fees?

A. Yes, fees associated with a specific purchase such as international transaction or currency conversion fees usually benefit from the same interest-free period as the transaction itself. As long as you pay your closing balance in full by the due date, you shouldn’t incur interest on these additional costs.

Q. Do you get interest-free days when you have a balance transfer?

A. Most cards don’t offer interest-free days when there is an unpaid balance transfer on the account. Just as there are no interest-free days when you carry a balance made up of purchases, there are also no interest-free days when you carry a balance transfer month to month. Once you have paid off your balance transfer, however, you can take advantage of your card’s interest-free days as long as you pay your closing balance each month and meet any other criteria set out by your card provider.

Q. Do you get interest-free days on cash advances?

A. Only purchases can benefit from interest-free days. When you use your card to make a cash advance transaction, that transaction will start accruing interest at your card’s cash advance rate straight away. It’s also worth bearing in mind that aside from not benefiting from interest-free days, cash advances typically attract higher interest rates than purchases, with a range of fees thrown into the mix too.

Q. Do additional cardholders get interest-free days on purchases?

A. Both you, as the primary cardholder, and any additional cardholders you choose to add are all linked to the same account. As long as you pay off your balance each month according to your card’s interest-free terms, both you and your additional cardholders will benefit from interest-free days on your purchases.